Call Us Today (877) 943-0100

How Do You Know a COI is Authentic? What Our COI Tracking Service Can Do

COI Management | February 27, 2023

Deciding to collect a Certificate of Insurance (COI) from the servicing companies you contract with is a great step forward. Now, you need to be sure that each COI is authentic, and knowing what to look for, what the common mistakes are and the typical areas that are overlooked can be the difference between a successful compliance program and one that only delivers false hope and risk. This blog will cover how you can tell if a COI is authentic and what to do if you need a COI tracking service to help.

For very specific reasons, we did not use the term “valid” with this blog when referring to the COI because an authentic COI may have expired, in which case it will no longer be considered valid. Our focus is on ensuring that each COI provided to your organization is not fraudulent and has been issued directly from the appropriate source, on the required forms, and with the expected content. Here are some basic items to look for when authenticating a COI. Failing to do so can increase the financial, reputational, and legal risk your organization faces. Below are key things to look for when reviewing a COI for authenticity.

Standard Forms Mean Consistency

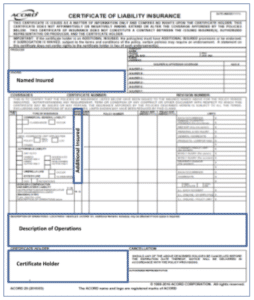

Most reputable insurance companies will provide their COIs on an ACORD 25 form. This is a consistent template that has been used for decades and looks like it! which allows information to be found quickly and in the same location on the form, no matter who issued it. It is a generic template with various boxes for information that at first glance, looks pretty simple. Since it is widely available, as are online editing tools, it is quite possible for less than honest companies to create a fraudulent version for their purposes.

Knowing the layout of the form and where certain information needs to be helps determine if you are being provided with an accurate form. Forms should also not appear to be photocopied, faded, or too dark as the form is standard in this regard. For example, the bottom left-hand corner of the certificate should say “Acord 25” and the top left corner has an Acord logo.

Most ACORD 25 forms have a set section for General Liability, Workers’ Compensation, and Automobile Liability. Other coverages, such as Cyber Security/Liability will be added on an as-needed basis only. If there is a N/A or $0 amount, this could be a red flag. This is not the typical layout as these areas are generally left blank on the form. If there is an entry like the above, someone other than an insurance professional likely completed the form.

The Named Insured box is at the bottom of the form. This should list the business name and address. Any discrepancies in this information could make a claim invalid as the Named Insured information must match directly with what is referenced in the claim.

The Producer information, which is the insurance company, should be on the form. The agent/broker information, who is the contact who created the document, should also be on the form under the Contact Name area, as well as their phone and email address. This contact name should also match the signature on the bottom of the form. Sometimes this information is missing or erroneously entered as the contractor’s information, which is a tip-off that the form is not properly issued.

Along the left-hand side of the form is an INSR LTR section, which is where the Insurer Letter from the “insurer’s affording coverage” should go. These indicate the insurance carrier for each policy. It is not uncommon for different carriers to be used for different policies and this information should be provided. At least one row must list a carrier and all coverages with limits listed have that letter in the INSR LTR column. If there is a letter next to an empty coverage section or this section is left blank, it may have been completed by someone who is not familiar with the form.

In this same area of the form, there are two additional columns on the left half of the COI stand for Additional Insured information and Subrogation Waived. The correct response on these is a Y rather than X. If there is an additional insured or waiver of subrogation listed in the Description of Operations box, the policy should have a Y in the column. If neither of these applies to the policies, they should be blank.

Look Closely at the Font and Format

Different agents will complete the forms in different ways, some are still completed by typewriters, and some may even be handwritten but the most important thing to look at is that whatever is used, is used consistently. There should not be a mix of different fonts and handwriting. There are consistent standards across the industry with how information is put on the ACORD form. There also should not be issues with alignment or the format of the actual form. For example, the effective and expiration dates should be in the middle of the box and in the same font as the policy number.

Ability to Verify the Contents of the COI

Any COI provided should contain the agent’s name and contacting them should result in a response and confirmation. If you cannot locate the agent, or they are not responsive when you try to verify information, this could be a cause for concern.

Insurance Company Should Be Legitimate

The insurance company providing the COI should be reputable and verifiable. Most of these insurance companies are rated and can be independently verified through sources such as www.web.ambest.com This insurance company information should be located on the top right of the COI and should be able to be found online and verified with a phone call or contact.

Summary

Whew! That is a lot for any organization to keep in mind, and tracking and missing even one piece could result in you holding a policy that is not authentic and will not provide coverage when you need it. We would be remiss if we didn’t acknowledge that sometimes mistakes get made, or information is missed, so not all deviations from the above are nefarious attempts to sidestep insurance requirements but in most cases, these forms should be completed properly and thoroughly. Over the years as a COI tracking service, PlusOne Solutions has conducted several audits for Customers reviewing COI’s and comparing them with licensed insurance agents. We know what each carrier’s standard practices are and can easily spot a really “good” fake COI from experience.

The good news is that there are professional COI tracking services, like PlusOne Solutions, who view hundreds of thousands of COIs each year and know exactly where to look for the important information, how the form should be completed, and what would be an anomaly. Partnering with experts like this can make your COI tracking process much stronger because the combination of human experience and technology creates an efficient and consistent process for managing COIs.

Contents are provided for information purposes only and should not be construed as legal advice. Users are reminded to seek legal counsel with respect to their obligations and use of PlusOne Solutions services.

About PlusOne Solutions

PlusOne Solutions has been an industry leader in the risk management field by specializing in compliance programs that meet the complex challenges of geographically dispersed contractors, vendors, and employee networks. PlusOne Solutions protects companies from possible financial, legal, and reputational risks associated with contractor and vendor relationships while creating safer work environments. To learn more, visit https://www.PlusOneSolutions.net.

To receive these updates directly in your email inbox, sign up for the newsletter. Questions or comments? We want to hear from you.

News

3 Signs It’s Time to Make the Switch from COI Tracking Software

Having COI tracking software can be an immense help if you were...

Read More

News

A COI Tracking Spreadsheet Can Come Back to Haunt You

If you have been searching for the perfect certificate of insurance (COI)...

Read More

News

An Inside Look At our COI Tracking Services

If you’re thinking about moving your COI Tracking services to a vendor...

Read More